Are you a part-time freelancer “stuck” in a full-time day job? Wondering how you’ll ever build your freelance business when you have to go to an office every day?

Are you a part-time freelancer “stuck” in a full-time day job? Wondering how you’ll ever build your freelance business when you have to go to an office every day?

You’re not alone. Thousands of aspiring and part-time freelancers are in the same spot. They need time to promote their services and to work on client projects. But they also need an income to support themselves and their families. Which means they need that day job.

How in the world are you supposed to break this cycle?

That’s the question that consumed me back in 2004. Quitting my full-time job to start and grow a freelance business wasn’t an option. I was my family’s sole breadwinner, so I needed that paycheck.

At the same time, I knew I was done with corporate America. I also knew freelancing was the right path for me. And I was certain that this was the time to start transitioning out of that mind-numbing treadmill.

So I decided to put a plan together. I stuck to my plan and made a lot of mistakes in the process. But 27 months later, I was ready. I had all the key elements in place. So I turned in my resignation… and I’ve never looked back!

In this article, I’m going to show you the basics of my plan and how to start freelancing when you have a day job.

Become a Venture Capitalist!

Let’s go straight to the biggest challenge most of us face when trying to make this type of transition: a steady income.

Quitting your job to start a freelance business would most likely mean going several months without a paycheck. And even if some freelance work came in, it wouldn’t be enough to cover living expenses for most of us.

So we need a way to replace that income safely. And until your freelance business can do that on its own, you need some sort of funding. You need start-up capital that can help you cover your living expenses during the leaner months and allow you to sleep well at night.

Essentially, you need venture capital.

Don’t worry, though. You’re not going to approach venture capitalists about investing in your business. Instead, you’re going to raise that capital yourself. And you’re going to do that by working your freelance business part-time and saving all your net profits after taxes.

In other words, you’re going to bootstrap!

The best thing you can do is keep your day job. That way you’ll still have income coming in and you can afford to stash away all your freelance earnings in a savings account.

Once you have enough capital stashed away to comfortably “fund” your business for a year (and once you have met other criteria, which I’ll share with you in a minute), you’ll be in an enviable position. You’ll be able to quit your day job and begin freelancing full-time.

This is the best, safest, and most reliable way to make the transition. It’s not theory or wishful thinking. I know it works because it’s exactly how I made the leap to self-employment just a few years ago.

OK, let’s get into the specifics of the plan.

Set and Track Your Key Milestones

In order for this plan to work, you’re going to need to set some key goals and milestones. These are critical, as they’ll guide your day-to-day decisions and help you determine how you’re tracking and what adjustments you may need to make as you move forward.

Your BHAG. The first thing you need to do is spend some time thinking about when you want to be fully self-employed—the actual date you want to go solo. This is important, because most of your other milestones and day-to-day activities will flow from this one milestone.

That’s why I call it your Big, Hairy, Audacious Goal (BHAG)!

In keeping with the spirit of the term, you want this date to be somewhat aggressive, but not so much so that it’s completely unrealistic and will set you up for failure. At the same time, it should get you excited and motivated. So choose a date that’s somewhere between thrilling and realistic.

Savings Reserves. Next, you have to determine how much start-up capital you’re going to need to make up for any income shortfalls during your first year. This is your safety net, and it will become the reserve account you draw from when you hit those lean months or when you have unexpected expenses (think broken furnace or refrigerator; it happens!).

How much you put away is obviously up to you. It should be based on your current resources, other sources of income (e.g., your spouse’s job), your financial obligations, and how much makes you feel comfortable. The greater your financial obligations, the higher the number. The more your family depends on your income, the more you’ll need.

Many financial experts recommend that families keep savings of at least six months’ living expenses. If you’re the sole breadwinner and this is going to be your full-time business, then eight to 12 months’ worth of living expenses may not be a bad idea.

That may sound like an impossible goal for you right now. But don’t get discouraged. Find a level you’re comfortable with. And remember: most of this amount will be funded by your part-time freelance earnings. I was surprised at how quickly our savings account grew once I started bringing in part-time work.

Your First Project. This is the date by which you want to land your first paid project (if you haven’t landed one already). This is important because that first paid project is the best thing you can get for your self-confidence.

What’s a realistic time frame for landing a first project? That obviously depends on the intensity of your promotional efforts, your ability to convert current contacts into clients, your profession, your chosen market niche (if any), and other important factors.

Here again (and with all these milestones), pick targets that will stretch you a bit and get you excited. Don’t be too conservative, but don’t be completely unrealistic, either.

Initial Monthly Income. This is the monthly income you want to start consistently earning as you work your business part-time (assuming that’s what you do during transition). You want to set a date by which that part-time income will be somewhat steady and predictable. When you reach this milestone, you’ll know that you probably have a viable business.

Trigger Monthly Income. This is the income that, when you start consistently earning it, will “tell” you that you’re ready to make the leap. This is probably one of the most important milestones to set, so let me explain what it is and why it’s so helpful.

Before going solo, I was earning about $10,000 a month in my day job. Because I had little spare time to work my freelance business (like most of you in this situation), I knew that my part-time income potential would be capped.

So then the question became, “OK, but if all I can manage to earn is, say, $2,000 a month from my part-time freelance business… how will I know that this would turn into a much bigger number if I were freelancing full-time?”

In other words, if my goal is to earn $10,000 a month as a full-time freelancer, what part-time income figure would turn into that number if I could work my freelance business full-time?

There’s no straightforward answer. It really depends on your profession and how much time you can afford to put into your part-time business. In my case, I set my “trigger” at $5,000 a month. In other words, when I consistently started bringing in $5,000 a month, that would be the indicator that the equivalent full-time effort would likely be $10,000 or more a month.

Number of Clients. Specifically, you should determine the number of clients you want to have and the dates by which you want to have them. This is not as important as the income milestones we’ve just discussed, but it’s still a good indicator of readiness.

In my case, I set an early goal of two clients and a longer-term goal of four to five clients by the time I quit my day job.

Health Insurance. If you live in the U.S. (and if you won’t have access to health insurance through another family member), it’s essential to start investigating your options early. Don’t wait until you’re about to resign from your job to start the process.

Take charge and investigate all your options—and how they may affect your ability to get affordable coverage.

I began the insurance search early, about six months before my target transition date (my BHAG). I also contacted an insurance broker three months before that date. I wanted to make sure I knew what I was up against way before I left my employer.

By the way, don’t try doing this alone. Contact an insurance broker and rely on his or her expertise. Good brokers know how to find the best options for your specific situation. Plus, you won’t pay any more to work with a broker than you would by going directly to the insurance company.

What If You Don’t Reach Every Milestone?

What if you’re rapidly approaching the end of your transitional period but haven’t yet reached all your milestones?

Use your savings goal as your guide. If you’ve met or surpassed your savings goal but your trigger monthly income is not as steady as you’d like it to be, that may be OK.

Ask yourself: “If I could do this on a full-time basis and therefore have more time to take on more projects and promote my business, how much more could I earn? Would that be a good starting point, even if it’s not my long-term income goal?”

In my case, even though I wasn’t hitting my trigger income every month, I was hitting some impressive numbers while working on my freelance business just 15 to 20 hours a week. I realized that if I could just leave my job and focus on this business alone, I could easily double—and probably even triple—what I was making on a part-time basis.

Tracking It All

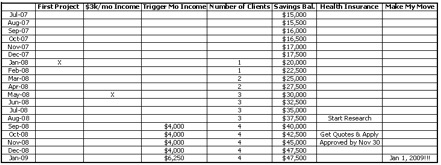

Now that you’ve set your BHAG and identified all your key milestones, it’s time to map it all out. That means putting it in writing and in a visual format you can easily track.

Putting your milestones in a chart, such as the one below, will help you see where you are today and what your journey will look like. It’s a good chart to print out and review every couple of weeks to make sure you’re on track. Plus, when you first run through this exercise, seeing your targets visually may also help you determine whether your goals are realistic or too conservative.

What Do You Think?

I’m the first one to admit that this is not the easiest path to take. But it’s the safest and smartest path when you don’t have the luxury of quitting your day job on a whim.

What do you think? Are you struggling to figure out how to escape the cubicle? What concerns you the most about making the leap to freelancing? What obstacles are you facing? What do you think of this milestone-based approach?

Please share your thoughts in the comments area below.